GLP-1 SHOCKWAVE

How Weight Loss Drugs Are Reshaping North America’s Economy & Your Health

Introduction: A Hunger Revolution Nobody Ordered

It usually starts with a pretty casual question in a client session: “So… what do you actually think about GLP-1s?” And honestly, there’s no short answer. Because what looks like a question about a medication is really a question about desire, willpower, identity, and what we’re willing to hand over to a pharmaceutical company in exchange for a smaller body.

GLP-1 receptor agonists which is the drug class behind Ozempic, Wegovy, Mounjaro, and Zepbound are not the “lose five pounds before your vacation” fix that social media has made them out to be. They’re powerful hormonal drugs originally developed for Type 2 diabetes, now prescribed at a scale nobody anticipated, on both sides of the border. They work by mimicking a gut hormone called glucagon-like peptide-1, which signals fullness, slows digestion, and fundamentally changes how your brain experiences hunger. For a lot of people, the appetite just… goes quiet.

And when appetite goes quiet at the individual level, the ripple effects are fascinating and genuinely alarming. People stop dining out as much. Wine bars close. Snack sales crater. Airlines quietly save billions in fuel costs because their passengers weigh less. And industries built on the premise of human hunger are scrambling to figure out what comes next.

But before we get into all of that, let’s name the thing that keeps getting glossed over: these drugs were never designed for casual or preventive use. The short-term wins are real. The long-term picture is murky at best. And the ways that healthcare systems on both sides of the 49th parallel are deploying them, some of which we’ll get into, range from creative to genuinely jaw-dropping.

This piece is co-published for both the Wellness Infrastructure & Altavita communities. Our perspective is the same regardless of the platform: we’re not anti-medication, but we are pro-transparency. GLP-1s are reshaping bodies, industries, and economies — and the full picture is worth understanding.

Core Uses vs. Misuse: What These Drugs Were Actually Built For

The FDA has approved GLP-1 receptor agonists for two things: glycemic control in adults with Type 2 diabetes, and chronic weight management in adults with a BMI of 30 or above — or 27-plus with a related health condition. Health Canada has approved them on similar grounds. These are serious medical situations, and for people who qualify, the benefits are real and documented.

Here’s how they work: GLP-1 agonists bind to receptors in the pancreas (boosting insulin, suppressing glucagon), the gut (slowing digestion so you feel full longer), and the brain — specifically the hypothalamus and reward centres. That last part is the big one. These drugs don’t just make your stomach feel full. They turn down the volume on the brain’s desire for food. Users often describe it as the “noise” around eating just… stopping. The constant background hum of “what should I eat, when can I eat, I want something” goes quiet.

The scale of projected adoption is staggering. Analysts estimate 30 million or more Americans alone will be on these medications by 2030, with Canadian uptake rising sharply as provincial drug coverage expands. Goldman Sachs has suggested widespread GLP-1 use could add a full percentage point to US GDP through workforce productivity gains. The global pharma market for these drugs is projected to hit $105 billion by the end of the decade.

The wellness take: GLP-1s used in isolation, without real nutritional support, movement habits, and behavioural work, almost always result in significant weight regain when people stop. And most people do stop, because these drugs are expensive, have real side effects, and weren’t designed for lifetime use (even if that’s increasingly how they’re being positioned).

We’re not anti-medication.

We’re just very pro-building-the-habits-that-last-after-the-prescription-ends.

The Moment That Says It All: Ozempic at the Olympics

If you watched Canadian Olympic coverage over the past few Games, you almost certainly saw it: Ozempic ads woven right into the CBC broadcast. Not a coincidence, and not a small buy. Novo Nordisk has been a recurring sponsor of CBC’s Olympic coverage across multiple Games, placing their appetite-suppression drug front and centre during the world’s biggest celebration of peak human athletic performance.

Let that land for a second. The Olympics are supposed to represent the absolute outer limits of what a trained, disciplined, nourished human body can do. Years of sacrifice, precision fuelling, movement as a full-time vocation. And sandwiched into that coverage, on repeat: advertising for a drug whose entire value proposition is that you don’t have to move ‘cause you won’t feel like eating.

To be fair, Novo Nordisk has framed their Olympic presence around the messaging that obesity is a chronic disease deserving medical treatment — which, for many people, it genuinely is. But the context creates a collision that’s hard to ignore. Elite athletes performing at the absolute peak of human capacity, and in the commercial break, the suggestion that the real solution to body challenges is a weekly injection. For Canadian viewers, this wasn’t a hypothetical juxtaposition. It was just… the broadcast.

The fact that this has happened across multiple Games without significant public pushback is itself worth noting. It tells you something about how thoroughly normalized pharmaceutical body management has become, that a drug company buying into Olympic glory barely registers as strange anymore.

Restaurant and Dining: When the Appetite Disappears, So Do the Diners

The restaurant industry has survived pandemics, recessions, and the delivery app revolution. The GLP-1 moment is different, because it’s not about external disruption — it’s about the customer themselves changing.

The most detailed data comes from the US, particularly California and New York, where GLP-1 adoption is highest and the restaurant industry is both densest and most closely tracked. GLP-1 users report dining out significantly less, ordering smaller portions when they do, and honestly finding meals less enjoyable overall. The social ritual of dinner still exists, but the appetite for it, literally and figuratively diminishes. One widely cited survey found GLP-1 users cut their restaurant visits by more than half compared to pre-medication.

Full-service restaurants in high-adoption markets are seeing year-over-year revenue declines of 8 to 10 percent. Fast casual is down 5 to 7 percent as smaller, protein-forward orders compress average ticket sizes. Even takeout and delivery, which everyone assumed was structurally bulletproof, is down roughly 7 percent in ordering frequency among GLP-1 users. Canadian operators in major urban markets are watching the same trends emerge, with a lag of roughly 12 to 18 months behind the US curve.

Restaurant & Dining Impact by Segment

Sources: Fortune, The Globe and Mail, NBC News, Food & Wine

The industry is adapting, because that’s what it does. Chipotle has been testing protein-focused mini bowls. Casual chains are quietly shrinking default portions while holding price points to protect margins. Fine dining is leaning harder into experience, the idea that you’re paying for an evening, not just a plate.

But there’s a ceiling on that adaptation. Restaurants run on volume. And a dining culture reshaped by mass appetite suppression doesn’t just change what people order, it changes whether they show up at all. The spontaneous weeknight dinner, the celebratory Saturday night out are appetite-driven decisions. When appetite is managed by a prescription, the whole behavioural architecture of “let’s go out” quietly erodes.

Wine, Booze, and the Beverage Bust

Alcohol and appetite share brain space. The same reward pathways GLP-1s dampen in response to food appear to respond similarly to alcohol — which is either a useful side effect or commercial disaster for the alcohol beverage industry, depending on where you’re sitting. (*Like the sober curious movement wasn’t already shaking things up!)

Clinical research is building around GLP-1s and alcohol use disorder, with promising early results. But the bigger market story isn’t addiction treatment, it’s the casual drinker. The person who used to have two glasses of wine with dinner and now nurses one. Or switches to sparkling water because the craving just isn’t there. About 45 percent of GLP-1 users in surveys report meaningfully cutting their alcohol consumption. Sixty-six percent report reducing their drinking overall. Great, right?! I mean on one hand yes, but industries will have to adapt.

In the UK, wine bars have already started citing Ozempic as a contributing factor in closures, and similar patterns are emerging in North American urban markets where GLP-1 adoption is highest. For wine bars, cocktail lounges, and premium spirits brands whose margins depend on beverage sales, the math is getting uncomfortable fast. Canada’s wine and hospitality sector, already navigating post-pandemic recovery and shifting consumer preferences among younger drinkers, is watching this trend layer on top of a market that was already in transition.

The non-alcoholic beverage category has been growing sharply across North America, driven by Millennial and Gen Z consumers who view reduced drinking as a wellness identity. GLP-1s are now accelerating a shift that was already underway, compounding the effect in ways that producers and distributors are only beginning to model.

Sneaky Economic Ripples: Industries You Didn’t Expect to Lose

Restaurants and wine bars are the obvious casualties. But the economic shockwave travels to some genuinely unexpected places across the North American economy.

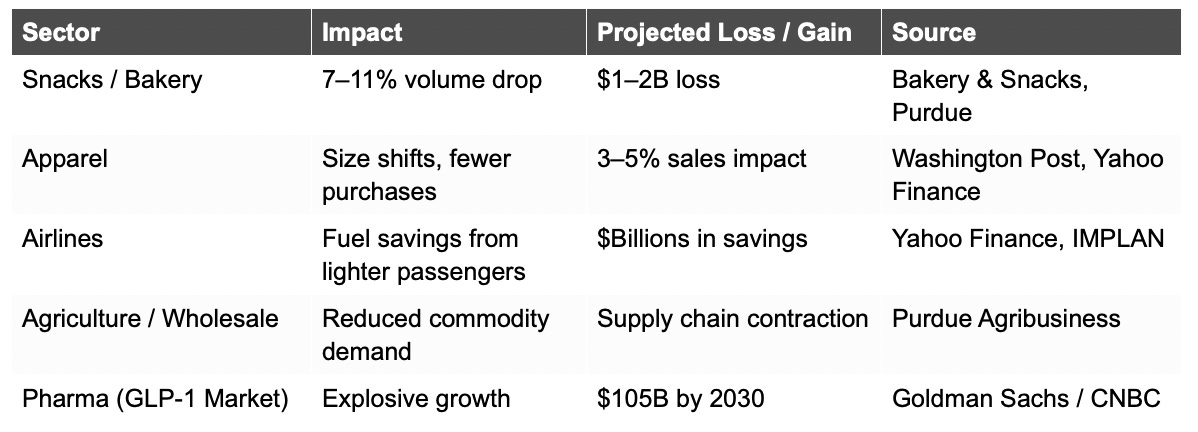

The snack and packaged food industry may be facing its most significant demand-side shift in decades. GLP-1 users essentially stop grazing, which is the between-meal eating that drives the majority of snack food sales. Cookies, chips, crackers, confectionery: all seeing volume declines of 7 to 11 percent in tracked GLP-1 user cohorts, translating to projected annual losses of $1 to $2 billion across the category. Major CPG players including PepsiCo and Mondelez have both quietly started reconfiguring product pipelines toward higher-protein, lower-volume formats for this consumer. Canadian grocery retailers are tracking the same category softness, particularly in centre-aisle snack and confectionery aisles.

Apparel is experiencing a subtler but financially real effect across both countries. GLP-1 users losing significant weight aren’t just buying smaller sizes, they’re often buying less overall, as their relationship with clothes and their body shifts. Plus-size categories are contracting without a corresponding uptick elsewhere. The sizing infrastructure of North American retail is facing an expensive recalibration.

Airlines on both sides of the border occupy a paradoxical position. Lighter passengers mean lower fuel consumption. With fuel representing 20 to 30 percent of operating costs, even modest average weight reductions across a passenger population translate to significant savings at scale. Air Canada and WestJet stand to benefit alongside US carriers in ways that haven’t yet made it into analyst models. The industry that has long been criticized for not accommodating larger bodies may end up as an unintentional financial winner of mass weight loss.

Agricultural supply chains, a cornerstone of both the Canadian and US economies, face longer structural pressure that hasn’t fully registered yet. Reduced caloric consumption at scale means reduced demand for the commodity crops that underpin processed food production. For Canadian agriculture, which still exports heavily into US food manufacturing supply chains, the downstream effects of reduced processed food demand are a slow-moving story that farm economists are only beginning to model.

Multi-Sector Economic Impact of GLP-1 Adoption

Sources: IMPLAN, Purdue Agribusiness, Yahoo Finance, Goldman Sachs/CNBC, Washington Post

Health Tradeoffs and Wellness Warnings: The Part That Doesn’t Make the Headlines

Let’s be clear: the cardiovascular and metabolic benefits of GLP-1 therapy for people who genuinely need it are real. For patients with obesity-related heart disease or poorly controlled Type 2 diabetes, these drugs can be genuinely transformative. But the risks that don’t make the Instagram infographics are worth naming plainly.

Muscle loss is a big one. GLP-1-induced caloric restriction, without proper protein support and resistance training, produces weight loss that is disproportionately lean mass. Research shows 25 to 40 percent of GLP-1-induced weight loss can come from muscle rather than fat. For older adults especially, that’s not a cosmetic issue — it’s a fall risk, a mobility issue, a metabolic issue.

Gastrointestinal side effects like nausea, vomiting, severe constipation, and gastroparesis drive meaningful discontinuation rates.

Long-term neurological effects of sustained appetite suppression on the gut-brain axis are genuinely unknown, because these drugs haven’t existed long enough to generate that data.

And when people stop? Clinical trials show average weight regain of 60 to 70 percent of lost weight within one to two years of cessation. Without the behavioural scaffolding, the eating habits, the movement practice, and the emotional regulation tools, the drug becomes a recurring dependency rather than a bridge to something better.

A Uniquely Canadian Problem: Ozempic on the Orthopeadic Waitlist

Here’s something that genuinely stopped us in our tracks. In Canada, where the public healthcare system runs under sustained pressure and orthopedic waitlists are among the longest in the developed world, a pattern has emerged: patients waiting for knee and hip replacement surgeries are contacting us at Altavita for quotes on immediate private solutions. They have told us that they are being prescribed GLP-1 medications to help manage their weight while they wait.

On the surface, that almost sounds reasonable. Excess weight does put additional stress on joints and can complicate surgical outcomes. But here’s the reality of what that actually looks like in practice: average wait times for knee or hip replacement in Canada are running at 18+ months or longer in many provinces. Eighteen months.

These are people who are in pain. Who can’t move well. Who are often sedentary by necessity because every step hurts. The medical system’s solution to “can’t exercise because of joint pain, waiting almost two years for the surgery that would fix it” is… a drug that suppresses appetite. Not a structured physiotherapy program. Not comprehensive pre-surgical nutritional optimization. Not a coordinated pre-habilitation plan. An injection to manage hunger while the clock runs down.

Let’s think through what that actually does to a body. Appetite suppressed, mobility severely limited, muscle use minimal — and we already know that GLP-1s can cause significant muscle loss even in active people. An immobile patient on GLP-1s for 18 months isn’t just losing fat. They are losing the muscle mass and functional capacity they’ll need to recover from major orthopeadic surgery and the rehabilitation that follows it. The drug prescribed to prepare them for surgery may be quietly making their recovery harder.

This is what happens when a powerful tool gets deployed as a system-level workaround for a resource problem. The intent isn’t malicious, clinicians are working within real constraints. But the outcome is deeply concerning. And it’s a version of a broader pattern playing out across North American healthcare: GLP-1s being used not as part of a comprehensive wellness strategy, but as a substitute for one.

The Bottom Line: Drugs Are a Tool, Not a Plan

GLP-1 receptor agonists are, by any honest measure, a remarkable pharmaceutical achievement. They are genuinely helping people with serious metabolic disease. They are reshaping the North American economy in ways that are only starting to be mapped. And they are raising profound questions about what we mean when we talk about wellness, appetite, and the relationship between human bodies and the systems: medical, commercial, and cultural that are built around them.

Ozempic runs ads during Canada’s Olympic coverage, nestled between footage of elite athletes pushing their bodies to the absolute limit. Canadian patients waiting 18 months for hip surgery are being handed a prescription instead of a pre-habilitation program. Wine bars are closing. Airlines are saving billions. A drug designed for Type 2 diabetes is being culturally reframed as a lifestyle tool and entire industries are being quietly hollowed out by suppressed human appetite.

None of that is simple. None of it is all good or all bad. What it is, is complicated and deserving of a lot more nuance than it usually gets.

Our take, across both Wellness Infrastructure and Altavita: these drugs can absolutely be part of a wellness strategy for people who genuinely need them. But “part of” is the operative phrase. The hunger signals these medications quiet are information. The habits they bypass still need to be built. The muscle they cost still needs to be maintained. And the person on the other side of the prescription still needs support that goes well beyond a monthly injection.

Sustainable wellness is built on habits, not hormones. If you’re navigating the GLP-1 conversation for yourself, a client, or someone you care about, we’d love to help you think it through. Explore Altavita’s retreats and coaching programs, and Megan Swan’s wellness strategy work, for support that lasts beyond any prescription.

| A guest post by

|